How and Why To Add Crypto To Your Portfolio of Goal-Based Strategies

Mathieu Hardy

Diversification has always been at the heart of effective portfolio risk management as it significantly reduces risk. Here is a look at why crypto might have a place in your portfolios.

A well-diversified portfolio contains a properly balanced mix of assets and asset classes. This commonly includes investments in the public equity and bond market, as well as real estate.

OSOM is the Crypto Wealth Manager to cover it all: wallets, exchange, Crypto Robo-Advisor, DeFi Earn to lend stablecoins in DeFi, and Crypto Strategie, it is all you need in a Crypto Asset Manager.

Our computers do the work for you with a long-term perspective so you don't have to. From crypto on-and-off ramps to passive income and diversified portfolios, OSOM has you covered.

If you are wondering how the Autopilot Works, read this. The live performance is here If you want to know why you might want to use DeFi Earn, read this.

The guide to getting started is here.

When you invest in the public market, you can only access public companies. However, the private market contains strong potential for great returns. The private market features startups big and small, but thus far, has mainly been reserved for venture capitalists (VCs) and private equity firms (PEs). Unfortunately, the costs associated with running a VC or PE fund mean these firms only raise big tickets from wealthy investors, and you don’t have access to them.

Recently, partial access to the private market has been granted to retailers through the phenomenon of equity crowdfunding in which a group of retail investors can collectively take a stake in a private company, though it is not widely used. Equity crowdfunding is arduous work for founders, given the lack of benefits associated with having experienced VCs on their board. And investors must typically wait five to ten years before exiting such investments, making them highly illiquid. And finally, crowdfunding often requires investments of several hundred to several thousand euros into one company. Investment amounts are significantly less than the investments of VC or PE firms, but they still represent minimal diversification when compared to what you’d get investing that amount in a fund that tracks the entirety of the investible public market.

Gaining access to the private market is difficult and while the good old 60% equity/40% bonds strategy may offer some diversification, it cannot protect a portfolio against systemic market risk as it is 100% invested in the public market. It’s not bad, but still not ideal.

For decades, hedge funds have looked for the perfect asset that can be shielded from systemic risk issues —an asset unaffected by volatility in the wider market.

For many, cryptocurrencies and the new use cases offered by blockchain technology offer an answer to these problems. A new breed of young companies seeking to disrupt entire sectors of the economy are upon us. You would typically find such companies in the private market while others offer entirely novel “values” which might offer greater protection against systematic market risk. They also offer the advantage of being liquid (the smallest cryptocurrencies still often trade in the tens of thousands of dollars per day) and are available at small amounts (you can buy most crypto with less than 1€), which enable you to build a diversified portfolio easily.

Although it used to be extremely expensive and difficult to break into a world where one could diversify broadly, low-cost index funds and crypto markets are rapidly democratizing access to diversification.

Welcome to a world where you can now invest like a hedge fund or a venture capitalist too.

Read below to find out how and why you should.

The Basics

Asset classes can be cash, equities, bonds, real estate, crypto, commodities such as gold or silver, art, watches, wine, vintage cars, and more.

Think Amazon or Solvay stocks for equities, US or Spanish bonds for public bonds, GE or Netflix bonds for private bonds, a house in Miami or an office building in Singapore for real estate, gold bars or silver ETFs for commodities, a Picasso painting, or a digital piece by Banksy for art, a Rolex for watches, Dom Perignon or Saint Emilion bottles for wine, a Ferrari or a Porsche for cars, etc. You get the gist - the list is endless.

Ideally, you want to diversify as much as possible across and within asset classes. But even with the promises of the new world, it can quickly grow expensive while some assets may even be entirely out of reach. For example, it’s fine to want to diversify by buying diamonds, but if you can only buy one whole diamond, you might need to sink all your money into it - then, you wouldn’t be very diversified.

You need to look at the asset classes which are accessible and attractive to you. Then, you’ll need to create the perfect balance of each asset class in your portfolio while diversifying as much as possible within each asset class.

Understanding assets & asset classes

Typically, the parameters you need to consider for each asset and asset class are:

- Returns: The amount of money is it likely to make you if any at all.

How much of a return on investment are you likely to see with any given asset class over the period you are looking at investing for? For example, equity markets have returned 8% to 10% between 1926 and 2019. The bond markets returned between 4% and 6%.

- Risks: What you could realistically lose at any point in time.

What is the loss you are theoretically exposing yourself to with any given asset class over the period of time you are looking at investing for? It appears equities are more lucrative than bonds. However, a portfolio with 100% exposure to equities could have lost as much as 43.13% in a year between 1926 and 2019, with 26 of 94 years representing a loss. For a portfolio with 100% exposure to bonds, the worst year was only 8.13% and only 14 out of 94 years experienced a loss. If you want the assurance that you will still have your money in four years, equities might be a little too risky - volatile - for you.

- Liquidity: How long does it take to get in and out of your investment?

If you need to sell your investments quickly for some reason, can you? This is really important to discern when considering asset allocation. If you need money in five years to purchase a house, it’s probably not in your best interest to invest with a venture capitalist who says any potential profits won’t come back to you for 10 years. Although you might become rich on paper after five years, you won’t be able to use any of that money since you can’t sell your shares to anybody. Equities, on the other hand, can be traded fairly quickly.

- Correlation to other assets and asset classes: How does an asset - or its asset class - move relative to others?

For most of the past two decades, a negative correlation with equity has meant that US Treasury bonds served as a hedge when stock markets tumbled. Bond prices typically rose when equities prices fell, therefore, balanced portfolios suffered smaller losses than portfolios with 100% exposure to equity markets. The idea here is that if you buy a lot of different assets, but they all behave the same way, you have, in fact, just bought a lot of the same thing.

- Price: What is the smallest unit of an asset you can buy?

If your goal is to save up to €50,000 to buy a car in five years, your portfolio will never be bigger than €50,000. Therefore investing your first €25,000 in a Rolex will mean that your watch is going to be between 100% to 50% of your portfolio. You won’t be able to diversify across asset classes - or even assets - with those price ranges for those types of assets. Even a share of Amazon (which costs €3,000) will make diversification difficult. But you can buy part of a bitcoin with only €50.

Building portfolios - Asset allocation

Now you understand asset classes and assets within those classes and that there are (at least) five things to look at when building a portfolio and choosing asset classes.

You want to look at different asset classes depending on your personal goals or objectives. And you probably have more than one goal or objective, so you might want to build several “goal-based portfolios”. A goal - and, therefore, a portfolio - will have a name, a target date, a liquidity profile, and a required minimum amount to reach.

Why is time important? Because in most cases, time will reduce your risks or make other factors, such as liquidity, less important. That is because a lot of assets are volatile and their trajectory is relatively unpredictable in the short-term but long-term trends are more predictable.

Take, for example, the equity market: knowing where a stock will be 2 weeks from now is very hard. But looking at historical trends, one can say that it is likely that over 30 years, the overall stock market will have gone up by an average of 6% to 11% a year. It’s not very precise, but it’s all “up”.

Here is an example of the average, minimum, and maximum annualized returns (%) when investing in developed world stocks between 1975 and 2017 (42 years), depending on the time horizon of the investment. Even when entering and exiting at the worst time, if the portfolio was held for over 25 years, it would have enjoyed a return of 6.4% a year.

The graph represents the average, minimum, and maximum annualized returns (%) when investing in the MSCI World equities index between 1975 and 2017, depending on the time horizon of the investment. Including dividends (total return index), in GBP. Those who held their investment for over 25 years would on average have made a return of 9.5% per year and even when buying and exiting their investments at the worst points in time they would still have enjoyed a return of 6.4% per year.

Another example: if you invest in art, it might not be a very liquid asset and you might not be able to sell it when you want to. But if you have 20 years ahead of you to see it appreciate and 10 years to sell it (a total of 30 years), then it's not quite as risky and you can better time your sale and also give yourself extra time to find a buyer willing to pay a good price.

A Goal-based approach to managing portfolios

You now understand that there are both assets and asset classes and that to build a good portfolio to achieve your objectives, you need to pick one or more assets in one or more asset classes.

So let’s talk about those objectives. Building portfolios per objectives is called “goal-based investing”. As a retail investor, you are probably not looking to “beat the S&P 500” or “generate 50% returns this year” but rather “have an emergency fund in case sh*t happens” or “make sure I have enough money for retirement” or “put my kids through university”. Those goals are going to have a name (so it’s easier to remember :) ), a liquidity profile, a target amount, and a target date. The liquidity profile, amount, and date will help determine the asset allocation.

Here is what Jane’s “goal-based” portfolio strategy could look like. Let’s assume she is 33, married, has 1 kid, and is looking to buy her own house in five years.

Goal 1

- Title: Emergency savings - Have six months of expenses set aside in case something bad happens

- Target Amount: €12,000

- When: As soon as possible

- Liquidity: Ready at a moment's notice

- Portfolio allocation: 100% cash

Explanation for the allocation: It needs to be liquid and Jane wants to make sure there is always €12,000 available if she needs it, so a savings account is the best place to put it. She will lose 2% a year to inflation which is fine - it’s a price she has to pay for security. It could be seen as a “bad” investment (because it’s constantly losing money) but it’s an excellent investment in regards to Jane’s stated goal.

Goal 2

- Title: Retirement

- Target Amount: €800,000

- When: 35 years

- Liquidity: Jane will need to draw the first money from it in 35 years, and after that, she still expects most of it will be invested until she draws money for the last time (statistically, 23 years later, when she passes away)

- Portfolio allocation

- 90% in a fund that tracks the entire world stock market, for example [IMIE.PA]

- 10% in crypto

Explanation for the allocation:

- It keeps Jane diversified when it comes to stocks for a very low cost (she can buy a share in that fund for €200)

- The crypto and startups allocation is to “boost” her returns if possible. The risk is limited because even if they all end up being worth 0 (which is highly unlikely, but returns could be bad, nonetheless), it’s just 20% of what she has.

- The startups are very illiquid, but she has 35 years before she needs that money. They should be a success or a failure by then.

- She doesn’t need cash, bonds, or anything else (for now) because equities are what has the best return profile and she has 35 years ahead of her and she knows she won’t panic if she sees -35% on her portfolio one year since the average return over 35 years should be about 10%. As she gets closer to retirement, she’ll switch some of the equities into bonds to reduce volatility, but for now, a very aggressive profile is all she needs.

- In a couple of years, she might change that allocation to add some art or real estate, but it won’t be much more than 1 to 2% of the portfolio.

- As she gets closer to retirement, (for example, 15 years prior) she will start thinking about slowly changing to more liquid and less risky assets.

Goal 3

- Title: Buying a house

- Target amount: €100,000 for a down payment

- When: In five years

- Portfolio allocation:

- 25% peer-to-peer lending

- 25% corporate bonds

- 50% EU government bonds

Explanation for the allocation:

- Jane doesn’t want to risk losing 30% of her portfolio in the year as she’s planning to buy a house, so she looked for relatively safe investments.

- She wanted something that would still beat inflation (otherwise she is losing money while she saves and while the real estate market is growing 3% per year).

- Bonds are always safer than equity since, in case of bankruptcy, lenders get paid before shareholders. And government bonds are pretty much the safest investment out there. Jane only chose EU bonds so she’s not exposed to any exchange rate risk.

Goal 4

- Title: Sending her kid to university

- Target amount: €150,000

- When: In 15 years

- Portfolio allocation: 100% in a fund that tracks the entire world stock market, so it’s diversified when it comes to stocks for a very low cost (she can buy a share in that fund for €200). For example IMIE.PA

Explanation for the allocation: Like her pension, it’s far off. But not quite as far, so she starts aggressively and will tweak the risk profile with time by buying more EU Government bonds instead of equities in 5-10 years and by selling some of the equity to purchase bonds instead.

So, every month, Jane will put some money towards those goals. She will start with the most urgent (emergency fund) and once she reaches that goal, she will start allocating money to the other three goals with respect to her asset allocation for each goal.

Why a crypto allocation?

Now that we’ve covered the basics of asset allocation and goal-based portfolios, here comes the highly-awaited question: why crypto?

For two reasons; there are two broad categories of crypto you can buy.

1) As a hedge against inflation and/or the devaluation of a currency and systemic market risk.

That’s what you are looking at with Bitcoin, Litecoin, or other such cryptocurrencies that don’t have a lot of utility but promise digital scarcity, similar to the way gold promises physical scarcity. Bitcoin and gold are both pretty useless (the gold that’s actually used “as a metal” is about 2% of the gold in existence, the rest just sits in bank vaults), but they are both rare and we ascribe value to what is rare. Bitcoin’s supply is fixed at 21 million Bitcoin. This means that buying Bitcoin can be seen as a way to “store value”. We can’t ascertain what it should be worth objectively, but we can see that it has gone from being worth cents in the beginning to above €45,000 recently - a strong indication that it is worth a lot to many. Maybe more than €45,000€; so not only could it help you “safeguard” value against inflation, but it might also make you a little bit extra money on top.

2) As an investment in startups building worldwide ecosystems.

That’s what you are looking at with Ethereum, Polkadot, Solana, Uniswap, Sushiswap, Maker, Near, etc... But there are still quite big differences between all those startups, similar as with all startups in the non-blockchain world.

Cryptocurrencies can have utility.

For example, on Ethereum, ETH is the “ticket” to participate in the ecosystem since you pay all the fees on that system with ETH whenever you want to perform an action on the Ethereum network. You can’t buy shares in the “Ethereum company” but you can buy ETH tokens hoping that, as more and more people want those ETH tokens to build and use decentralized applications, their price will appreciate.

You can think of it as Amazon Web Services (AWS) if what was needed to pay for their service was the “AmazonCoin”. If you were able to get your hands on some “AmazonCoin”, a lot of developers would come asking you to sell it to them so they could build applications on the Amazon Web Services platform.

Other cryptocurrencies are used as voting right in the protocol and access to some of its profits.

For example, Sushiswap has a token, SUSHI. Sushiswap is a decentralized exchange - like the Travelex booth at the airport, but for crypto and totally run by computer code. Whenever an exchange happens, the Sushiswap protocol collects a 0.05% and gives it to people holding the SUSHI token in the Sushibar (I know 🙄). You can think of it as a dividend from a share in a company. So far, (since mid-2020) they have collected $114,193,129 in fees.

Additionally, also like a share in a company, if you hold SUSHI tokens, you can vote on “governance proposals”. Unlike in most companies, it’s extremely transparent.

There are hybrid models

Governance tokens that don’t pay out fees, utility tokens that also afford governance rights, and a whole host of variations. Before taking part, it’s important to understand the ins and outs.

The bottom line is - you want to diversify. And if you still have many years left in your life, it would be wise to take on some measured risks. And you can only look at assets where the “entry ticket” (the smallest possible portion you can buy) is small enough so that you can afford to diversify.

So that’s “why crypto”.

How can you add crypto?

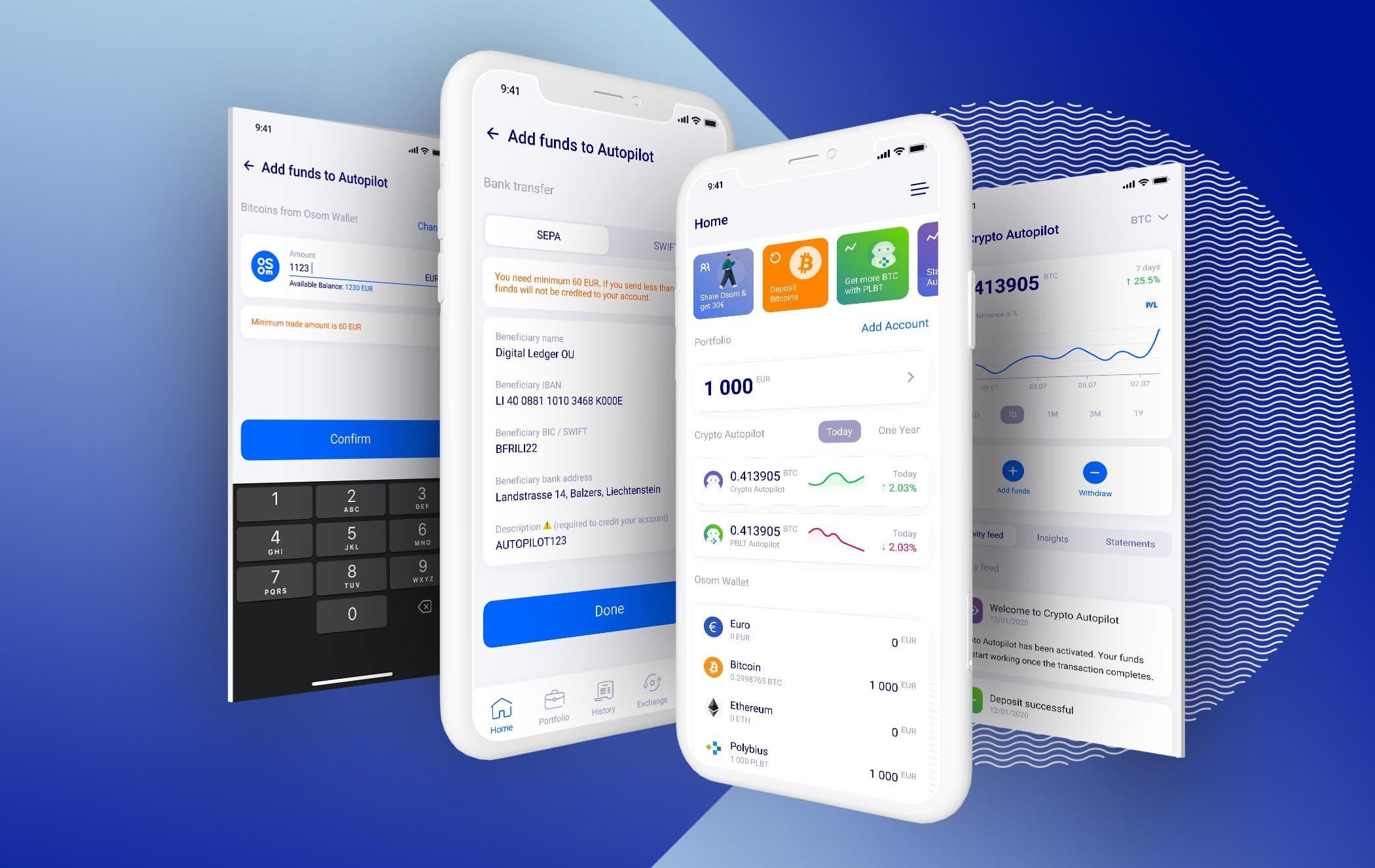

With OSOM you can buy Bitcoin starting from €46, you can buy Ethereum starting from €31 and you can deposit in the Autopilot from €100.

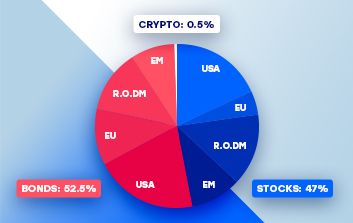

The Autopilot offers a very diversified portfolio of cryptocurrencies of all types. We track over 200, have had between 40 and 55 investible at any given point, and the Crypto Autopilot usually holds 9 to 14 at any given time, rebalancing up to every 15 minutes to ensure the ideal portfolio. And you can invest in the Crypto Autopilot on auto-pilot

If you decide to put €100 a month in the Crypto Autopilot, this gives you the opportunity to add digital stores of value and access some of the most exciting and revolutionary startups in the world for the price of one beer a day. This is something that would have been unthinkable a few years ago. Today’s world is more exciting than ever for retail investors.

This is not investment advice, nor a solicitation. Crypto markets possess a high level of risk, including volatility and regulatory uncertainty. Past performance does not constitute a guarantee of future results in any way. You are solely responsible for doing your own financial, legal, tax, or investment research before taking any actions.

Mathieu Hardy

Would you like to be notified about new posts?

Related articles

This step-by-step guide will walk you through the whole process of using our app, from depositing funds to getting started using the Autopilot.