Optimistic on all things crypto | The OSOM Thesis

Mathieu Hardy

When numbers go up, everyone is a genius and no one needs a thesis. It’s when numbers go down and doubt seeps in that we need to remember why we invested in the first place.

There are near-inescapable forces at play:

- (1) bits are cheaper & more rewarding to manipulate than atoms, and so software eats the world.

- (2) Blockchains are amazing coordination machines

- (3) Decentralization offers more agency vs Big Tech & Big State

=> Blockchain is unstoppable software that will eat the world.

It's developing in much the same way as technology before it (maybe only more publicly) :

- (1) following the hype-cycle (Gartner)

- (2) disrupting from the bottom up (C. Christensen)

- (3) with clearly identifiable feedback loops

=> Nothing new here. Except for the fact that for the first time you too can be early.

Prices are distracting, and largely meaningless in the short term.

For the first time everyone has access to the potential upside of high-growth tech startups. But to take advantage of the opportunity you need to ignore the noise of short term prices and find an intelligent way of getting exposed to the ecosystem. That's OSOM.

More details in 4718 words below 👇

Introduction

It’s well documented that investors are likely-er to stay invested in a portfolio they understand.

In that spirit, we thought now might be a good time to re-explain our thesis for investing in crypto assets. After nearly 7 months of almost constant price decline and several bankruptcies of centralized crypto firms, we see doubts everywhere. When money leaves the market, usually so do beliefs, and that’s why as humans we are more likely to invest when the numbers go up than when they go down. “Narrative follows price” and humans like stories. But this has also been documented to be the worst way of investing. So let’s leave prices and narratives aside for now, and focus on the larger arc of history. For context, OSOM started in 2017 with the Polybius ICO. The team wasn't born from last year’s hype.

Now’s a good time to sit down, take a pause, and articulate our thesis for crypto - and our reason d’être - again. There’s less noise, less optimism, less FOMO, and fewer grifters. It’s a better time for thinking.

We will start by looking at the unstoppable force of digitalization and the appeal of decentralization as the major undercurrents that are powering the natural move to Web3. To understand why this natural move does not appear to be following a straight line, we will look back at theories of tech cycles and disruption. We will conclude with a reflection on prices and our approach.

And just so we’re clear: none of this is very original thinking. It is merely a collection of other people’s thinking on the topic of tech, disruptive innovation, and adoption. We’re just trying to be helpful by aggregating it all. It’s also not financial advice, it’s for information purposes only.

We’ll stay high-level and won’t deep dive into specific assets or examples here, but we’ll put out an accompanying piece that details some of the use cases we see today and tomorrow.

The unstoppable forces: Maximum Value, Maximum Freedom

Everything that can become digital will become digital

That’s what history tells us and we have no reason to think that will stop anytime soon. One could argue that “crypto” is just the next logical step of the internet. After having digitized and then digitalized(1) much of our “information” world, all the value also gets digitalized. That is why “web3” is often used interchangeably with “crypto”.

This unstoppable movement to digitalization is fundamentally driven by the rational choices of economic actors looking to minimize their costs and maximize their opportunities.

Bits Over Atoms

Bits are cheaper to handle and infinitely more malleable than atoms. Bits, in fact, mostly have a zero marginal cost.

Here is an example:

A digitized invoice, in PDF format as opposed to paper, is immensely more practical to have than the printed-out version. But that is still very skeuomorphic and it doesn't leverage all of the advantages of computers. As can be attested by the fact that we had to develop OCR (optical character recognition) software to read those PDFs to automate accounting. But when you think about what is actually useful information in an invoice, it could very well be served like a webpage or in XML, and be natively machine readable.

Much of our lives has already been transformed into bits: news, emails, music, movies,...

Source: https://i.pinimg.com/originals/f2/2a/cf/f22acf9b72df247df7f91935490e19a8.gif

But much of our lives have not yet been. Because computers are amazing copying machines and we didn’t yet know how to create digital scarcity. We only knew about digital abundance. Stocks, Bonds, Real Estate, Hotel and Concert tickets, money, etc...are all digitalized today, but are not digital. Clearstream keeps track of stocks and bonds as if they were PDF copies of the paper of the past. Real Estate records are maintained in centralized ledgers by the states in what is essentially the Excel version of the leather books they used to have. Your concert ticket is just the PDF rendition of a centralized booking database with a QR code that links to that same database for convenience. The bank issues you money by typing numbers in a computer as opposed to writing it in a big book, but the process hasn’t changed, and “clearing” the books with other banks can still happen only about twice a day because they don’t share much infrastructure. All of those are like the PDF version of invoices: more practical than paper, but retaining much of the attributes of paper and gaining almost no “digital” characteristics.

Up until now, there were no good solutions. But crypto solves that. Your shares can be a fungible ERC20 or ERC1404 token. So can your Euros. Your invoice can be an ERC721, also known as NFT. So can your concert ticket or hotel stay.

This makes them cheaper, more transferable, and more useful. So it will move there. And it will make the first wave of digitalization look very small in comparison. There is no telling how quickly it will happen but that has been the direction of history since the invention of the Telegraph. Until we find a better technology than blockchains to create digital scarcity, that’s where our bets will be.

Coordination Advantage

In a pre-digital world, you have shareholder general assemblies and building co-op voting and vote tallying done with everyone in a big room holding up hands or writing on little pieces of paper.

In a digitized world, because Covid struck, those assemblies are held over Zoom. But it’s the same meetings, with the same agenda, held at the same pace, and they check identity & ownership the same way as in the pre-digital world.

In a digitalized world, Decentralized Autonomous Organizations have all their token-holders vote asynchronously as often as needed.

Imagine the opportunities for direct democracy.

And seeing as though there isn’t the problem of databases that can’t speak to one another anymore, your community is de-facto global. And you can pay your contributors globally too, without ever wondering if they have access to a bank account, because now everyone does, and whether your bank will have correspondents that will manage to get money over there.

The technological primitives also allow for more rapid iteration, more ownership and upside participation for the users, new governance and economic models, and more liquid and efficient capital markets.

Crypto has no regard for the artificial nation-state barriers and existing local monopolies. It is credibly neutral and de-facto global. It offers the option of “opting out” of your local circumstances to a degree, greatly mitigating the effects of the “geographical lottery”. It is therefore likely to win (but not without challenges). It’s, in fact, hard to see a world where all this tech is NOT playing a role.

"Software is eating the world" -- Marc Andreessen, 2011

Or, from Gartner in 2021

The Appeal of Decentralization

Before we dive into it, let's address a common criticism. Much of the comments thus far have revolved around "why would I need that", or " I can use Paypal/my bank/Transferwise to send money". And yes, you probably can. But there are billions of people that don't enjoy your level of freedom or legal certainty and (relative) currency stability. There is also nothing that absolutely guarantees that you will continue to enjoy those privileges forever.

If globalization was the bringing together of the world's countries and conglomerates, decentralization is the bringing together of the world's people. There is a reason why you hear so much about "community" in Web3.

While critics speak of "atomization" (everyone going back to his own little individual self), the careful observer will notice that Web3 is full of communities around shared projects. People meet and collaborate at an incredible rate.

What the critics call "atomization" is probably just lamenting that individuals are opting into shared communities as opposed to being forcefully enrolled into the communities of old (religions and nation-states, for example).

The reliability of math and the option to "(build and) choose your own tribe" are offering a compelling alternative (substitution) for the diminishing trust in existing institutions (see Messari's first part of the #1 thesis for 2022).

Versus "The State"

In a Volatile, Uncertain, Complex, and Ambiguous (VUCA) world, having assets that are "out of this world" offers some comfort as a "fallback" in case the proverbial sh*t were to hit the fan. Portable digital private property that can't be stopped and is accepted worldwide is already a compelling enough reason to stash some money on a blockchain as opposed to under your mattress. If your local institutions turn unfriendly and you can make it out, a 12 words seed phrase is a lot easier to carry than a backpack full of gold or bills. If the company your work for is "in the clouds", unincorporated, and pays you in a globally accepted asset, you are much less likely to be at the mercy of your local dictator.

In that regard, Bitcoin is a property right. It's a little unsure what it might be worth but it's unlikely to be worth 0. And you're pretty much guaranteed (at least today) to find a buyer anywhere in the world. It's the most portable and non-seizable property that exists (if you self-custody).

States are in the business of creating public goods(2) but don't create private property. They often help safeguard it but have also been known to seize it. So it makes sense to look to non-state actors for safeguarding digital scarcity.

As it is unlikely that the 184 governments of the world will be able to collude to ban self-sovereign blockchains (seeing as though they have never managed to coherently collude on anything thus far), it makes for an interesting new "balance" in the new world order.

Versus "Centralized Big-Tech"

Centralized "Big-Tech'' has obviously gone too far. We don't need anything else to make the case than to tell you to look at the EU commission and the USA Congress's take on Facebook, Google, and Apple.

Regulators have tried forcing centralized tech companies to make data portable from one system to another, to make them acknowledge that they are custodians of your data but do not actually own it and that you should be free to do with your data as you please.

It's pretty obvious that it's not working. When you can export your data there is nowhere to re-import it to. You pretty much have 0 visibility in real-time on who has what data about you, and getting data to be removed from processing is no walk in the park.

Having to beg your bank to share your identity with another provider, or having to ask Facebook to know who your friends are, does not make one feel like they have much agency.

The bottom line is that between the legacy tech and the entrenched interests, it's better to leapfrog them than to try and bend them to do something they weren't built for.

Web3/Crypto allows for you to own your social graph, reveal truths about yourself without revealing information (zero-knowledge proofs), allows for portable identity and reputations systems to be built, and for all of that to be in your control. Including the ability to delegate that control if it's too much work, and to take it back if you're not happy with the service.

The (Immovable) great constants: Tech Cycles and Disruption Theory

Thus far in this article, we have seen that:

There is an economic incentive to digitalize everything; to minimize costs and maximize opportunities.

There is also a political incentive to guarantee oneself maximum freedom and option, be it freedom from state or tech "tyranny".

So why is there not a straight line from here to there? The answer is an interesting mix of human psychology and market forces. Let's start with frameworks that attempt to explain what we're seeing, and why it looks like things we've seen before.

Gartner’s Hype Cycle

The Hype Cycle is the graphical representation of how technologies mature and get adopted through 5 phases, over time, while being more or less "visible" to those not actively working on it.

It is undeniably a simplification but it provides an interesting "grid" through which to interpret the world. This is how the story goes: a new technology comes to the fore, is widely presented in the media and popular culture, and we collectively get to thinking it is going to solve everything. But it doesn't actually do much yet. Once the "overinflated" promises don't immediately materialize (and some outright scams blow up in everyone's faces), we collectively lose patience and hope. But some true believers stick through it and keep building even when no one is paying attention. After a while, their solutions come out and they are actually usable, and good. It doesn't solve everything but it solves a lot of things. They get adopted by the majority and become the new normal.

Some technologies go through this really quickly. Others take decades. Some get a lot more attention than others in public media while some are important in some very niche media only. Some tech dies along the way and never actually makes it to the plateau of productivity. But pretty much all the "tech" you've ever encountered has gone through this cycle: your car, your TV, your phone landline, your personal computer, your grandparents' cassette player, your smartphone, streaming, fintech,...

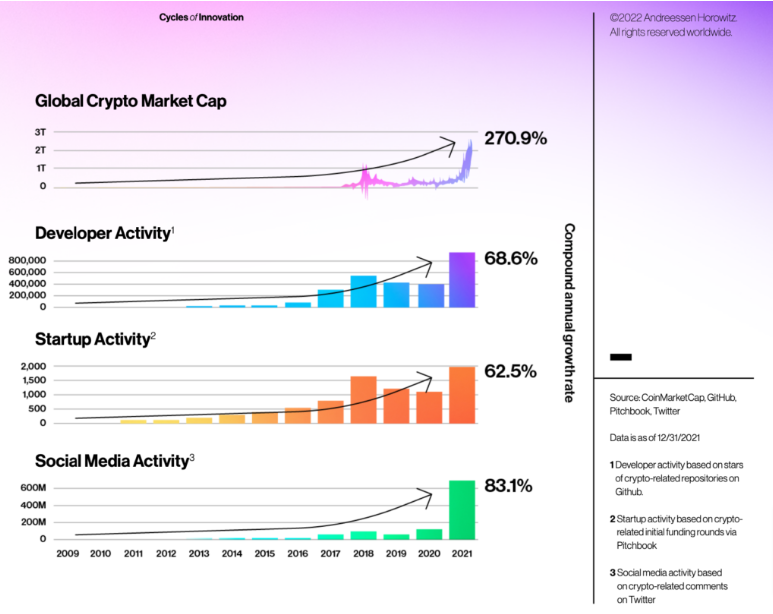

Blockchain, Crypto, Metaverse, DeFi,... are all going more or less quickly through this cycle too. Here is what Gartner published in mid-2021.

It's been said (but the quote is attributed to many people) that "any new technology tends to go through a 25-year adoption cycle. This makes sense since that is about the span of a generation. The people who adopted "a" tech early just grow old with it and their kids consider it to be a normal part of their lives.

There is however a bit of a variation in that timeframe because some technology is more "fundamental" than others, and as technology advantages compound, you can build on the previous tech to spread the new tech. Web2 didn't have Web2 to help it propagate. Web3 does.

But there are some constants too, like the rate at which humans learn and are willing to try new things.

Clayton Christensen’s theory of disruptive innovation

The Hype-Cycle is a useful simplification for thinking about the trajectory one technology takes. But how do technologies and businesses evolve relative to each other?

To answer that question, we can turn first to Clayton Christensen’s theory of disruptive innovation. Let’s quote the HBR article’s quick recap of the idea:

|| "Disruption” describes a process whereby a smaller company with fewer resources is able to successfully challenge established incumbent businesses. Specifically, as incumbents focus on improving their products and services for their most demanding (and usually most profitable) customers, they exceed the needs of some segments and ignore the needs of others. Entrants that prove disruptive begin by successfully targeting those overlooked segments, gaining a foothold by delivering more-suitable functionality—frequently at a lower price. Incumbents, chasing higher profitability in more-demanding segments, tend not to respond vigorously. Entrants then move upmarket, delivering the performance that incumbents’ mainstream customers require, while preserving the advantages that drove their early success. When mainstream customers start adopting the entrants’ offerings in volume, disruption has occurred. ||

As is clear from the quote, the disruptor’s offer is often a lot worse than the existing state of play for most people. To the mainstream, it will often look like a toy. Just like digital cameras took crappy pictures initially. Or how clunky it is to make a transaction on Ethereum and need to pay gas fees to a network.

But to some of the market, this new "toy" makes something previously inaccessible accessible. Or it enables radically new use cases. This is very much in line with Gandhi's famous quote: "First they ignore you, then they laugh at you, then they fight you, then you win."

Digital Cameras allowed you to take crappy pictures, but you could now take pictures of absolutely everything all the time. Sending tokenized US Dollars on the blockchain is a lot less convenient than using Venmo but there are now 7.5 billion people who don't have Venmo that can finally get some USD, when it was previously unthinkable.

Bitcoin is a lot more volatile than the Euro, so why would we use it? Well, maybe it's not much use to us, but in Argentina the IMF WEO reported a 3-year cumulative rate of inflation of 216% as of December 2021 and a forecast annual rate of inflation of 48% for 2022 and 42% for 2023. And in Lebanon, The IMF WEO reported a 3-year cumulative rate of inflation of 173% as of December 2020, but noted that "for Lebanon, data and projections for 2021-27 are omitted due to an unusually high degree of uncertainty. Venezuela remains hyperinflationary with the 3-year cumulative inflation rate in excess of 2,330,000% in December 2021 and a forecast annual inflation rate of 500% and 500% for 2022 and 2023, respectively. If those are the economies you live in, Bitcoin's volatility is much less of a concern. And the fact that it's a clunky experience to get your hands on some tokenized US Dollars won't deter you very much.

Crypto was meant, amongst other things, to increase financial inclusion and offer robust services in a low-trust environment. That is definitely an overlooked segment.

A16Z’s innovation cycles

The Hype Cycle presents how technology usually goes from discovery to acceptance. And the theory of disruptive innovation explains how most radical changes in industries start in the low end of the market with sub-par products to previously under-served participants. To complement the understanding, it is useful to also call on one venture capitalist’s look at what is happening to the crypto ecosystem in particular.

A16Z’s vantage point is interesting: Marc Andressen and Ben Horrowitz were there for the birth of the internet with the first major browser, Netscape. They then started investing in tech companies and were one of the first ones to invest in blockchain & crypto companies. They have described the inability to natively move value over the internet as its “original sin”. And they see crypto as the best way to remedy that and take the internet to its logical conclusion of being the network for everything.

When it comes to crypto, they have theorized the existence of identifiable innovation cycles. In their view, the increase in prices brings more interest to the space, which leads to new ideas and new projects being funded, and the cycle to start over. They call it “the price-innovation cycle”. And even though it all seems very chaotic and volatile, it is possible to discern this underlying logic. And the feedback loop, over time, fuels long-term growth.

And to those who would not find it sufficient - and although there are plenty of examples, wish to display their lack of research by asking repeatedly "where are the use cases?" - we can say this: To a large degree, that question is entirely irrelevant. When Tim Brenner-Lee invented the WorldWideWeb he had no idea what you'd be able to do with your phone in 2022. And those that venture into making predictions (like Ray Kurzweil, who claims an 86% accuracy rate with his predictions going back to the 90s) are often laughed at because they sound outlandish when made.

Much like with the internet and the GPS, a system of permissionless innovation and composability will enable unpredictable use cases. What we are able to predict today is but an extension of what already exists because we are very bad at thinking exponentially and in compounding returns. The next 7 years of building with blockchain and smart contracts will undoubtedly bring more use cases than the first seven. Because, like interest, innovation compounds. We obviously need to be able to see a road from "here" to "there" without resorting to "magical thinking", but we believe there are more than enough examples to do so (see this article for examples).

Web(2) was called a bubble because it had lots of users and no business model (money). Web(3) gets called a bubble because it has lots of business models (and money) but no users. It's reasonable to assume that, wherever you start, one tends to attract the other. It's uncertain, but it isn't unreasonable.

Prices are Distracting

Software eats the world. Self-sovereign, permissionless, and decentralized economies offer an alternative to yesteryear’s institutions. Decentralized Autonomous Organizations are speedrunning governance and offering new tools for collaboration on a planetary scale. The spread of those new paradigms follows a historically pretty well-charted path in how they are perceived and adopted. Even the peculiarities specific to crypto are theorized by now.

But oh, my! the prices, look at the prices! It moved! Did you see it move? Oh my god, it’s moving so much today!

Yes. It moved. If you read any of the points above you will have understood that we are very much at the beginning of everything. Crypto people say “we are early”. Yes, it is early. And we don’t see a lot of pension funds investing massively in crypto and crypto companies, what we see are Venture Capitalists and individuals. That is because at this stage blockchains and blockchain apps are (de)centralized liquid high-growth tech startups (or at least that’s the best analogy). They are crowdfunded and funded with venture capital. Just like most other entrepreneurial endeavors.

“De” is between parenthesis because the operations aren’t always quite decentralized, sometimes the ownership is not either, but it is definitely accessible in a decentralized way (ie: uniswap). And is often on the way to decentralization.

The difference with so many of the high growth-tech startups of the past is that they are (1) available for anyone to invest in, whereas it used to be only Venture Capitalists (VC) who could invest (2) liquid, meaning you can pretty much trade any of them at any time; whereas VC positions used to be somewhat illiquid and almost never publicly traded.

This is great because it is giving a lot of people the possibility to invest into high-growth tech startups, but the nature of the investment - it’s early and risky - means that it is also the first thing to be sold for cash by those who want to take fewer risks when times become more uncertain.

The fact that that price point exists is leading people to believe that it’s important and they should be looking at it. Whereas if they are investing like VCs, with a 5 to 10-year time horizon, they really shouldn’t. Because the price will likely move for a whole host of reasons that has nothing to do with the intrinsic value of the undertaking

This is the psychology of a market cycle. It exists everywhere, and it looks a lot like the Gartner Hype Cycle, except it happens much faster and not necessarily in parallel with technology development. There is usually a trigger, but it can be many different things.

Karen Bennett, writer at cheatsheet.com, has the created the amazing chart (above) showing the psychology of a market cycle. It describes the most common emotions people experience as the market fluctuates. These human emotions drive our financial markets much more than the market fundamentals.

What one must absolutely avoid is repeating this until they are broke.

Looking at crypto prices makes it hard to resist the temptation, because those numbers feel meaningful, when in fact - in the short term - they aren't.

What is important is to have an investment thesis, a time horizon, and the conviction to hold your portfolio through it all to resist the mind('s) tricks.

Many called Facebook crazy when it acquired Instagram for 1 Billion, and between 1999 and 2001 Amazon's stock plummeted 92%. And that was in the public markets. Since those lows, Amazon is up 19’340.57%.

In 2018 the price of most Cryptos crashed hard, while the rest of the market was doing pretty well. At the time there wasn’t much you could “do” with crypto. No “market-fit”, so to say. Since November 2021, it is crashing because there may have been a bit of a bubble, but there were bubbles everywhere, and because everything else is crashing too. But the situation is undoubtedly different. You can do things in and with crypto. It’s visible, if anything, because regulators are stepping in. You can’t say Crypto is useless and unscalable and at the same time want the regulators to limit the use of stablecoins to € 200m a day in transactions. If regulators feel it should be limited, it’s because they know it might be very appealing.

So beware of the prices, they don’t tell the full story. If you agree with our arguments in “unstoppable force”, understand the naturally slow uptake, and learn to recognize the market cycles for startups, you may get to enjoy the rewards when it finally works out.

Take it from Gartner, from July 2021

OSOM's Value Proposition

For the first time in history, everyone with a little money has an opportunity to expose themselves to high-growth tech startups. It used to be the reserved hunting ground of VCs and you needed a lot of money to participate. But in this field, you don't.

It used to take 100'000 dollars to become part of a VC fund. It takes €100 to get a diversified portfolio of crypto assets. That's because they are liquid and very fractionable.

It's quite probably not where you should put all of your money. But some money doesn't seem unreasonable for most investors. If and how much is a decision you should make with your financial advisor, we don't advise.

The approach we are taking is that we are 100% convinced that the addressable market is enormous and that there is tremendous value to be created and captured by crypto. We also know that trusting anyone to pick the winner is unlikely to work.

For comparison, In the 1800s you could have been directionally correct that cars were going to be a huge technology that was going to change the world and still gone completely bankrupt by investing in the wrong car companies.

And even today most active managers don't outperform the benchmarks (here is just one such example).

Our approach is to go for a broad swath of the "mid to top market".

It's too risky to be investing very early in tiny little projects that aren't liquid.

But it's not necessary either to wait until they are all 100% mature and considered "normal" to take a position in them. Our opinion is that the ideal time to consider them is when they've been derisked a little, but when they're still some (as of yet unfulfilled) promises, because that's where outsized returns are made.

So we have elected to choose a pretty broad universe of tradable crypto assets and to let an algorithm watch the evolutions and take diversified positions as it sees fit. It keeps up with trends before we really notice them and ensures a "non-emotional" approach to managing a portfolio of long-term bets on the space. It is neither a passive index - which is dangerous and we cover here - nor an actively managed portfolio because humans are unreliable.

Our opinion is that, when looking at innovation, you need to take a "portfolio" approach. That's because it's risky and approaching it as a portfolio spreads out the risks. That's what VCs do, as they usually expect 1/10 company in their portfolio to actually survive. That's what innovations teams (should) do in large companies as the chance of success of an innovative project in the market is not much higher than that of a startup.

Despite our confidence in this future, prices might not reflect what we believe are the fundamentals at all times. As legendary economist Kenyes said, "Markets can remain irrational longer than you can stay solvent". So you might want to consider making sure to never ever have money you need for something else deployed in the markets. Any markets.

Footnotes

(1) while digitization is the act of getting material into zeros and ones, digitalization is about creating native digital assets. So, whereas an e-book is a digitized book, Wikipedia is a digitalized (or digital) encyclopedia. The process by which Wikipedia came to be is unfathomable in a physical world. If you had to reprint Wikipedia every time someone made an edit, you would very quickly run out of paper.

(2) From Khanacademy: A public good has two key characteristics: it is nonexcludable and nonrivalrous. These characteristics make it difficult for market producers to sell the good to individual consumers. Nonexcludable means that it is costly or impossible for one user to exclude others from using a good. Nonrivalrous means that when one person uses a good, it does not prevent others from using it.

Mathieu Hardy

Would you like to be notified about new posts?

Related articles

The Crypto Autopilot looks at several months of past price data to build a portfolio for the medium to long term (2.5 to 5 years) with the objective of achieving stable growth - which means avoiding drawdowns.