Quantitative Investment Strategies - From Wall Street to Your Street

Mathieu Hardy

Previously reserved for hedge funds and other large financial institutions, quantitative investment strategies are increasingly becoming commonplace among retail traders as well.

Quantitative-based trading, or simply quant, relies on mathematical or quantitative modeling of the markets. In essence, quant is applied mathematics to the stock market, analyzing all available technical indicators for risk management and calculating potential returns.

To assess the "true" value of stocks, quantitative strategies rely on both historical data and real-time trading prices. This way, the quant approach to portfolio construction aims for so-called alpha returns - ones that beat the market average returns. Suffice to say, this is an enticing prospect for investors, but one should consider downsides as well.

OSOM is the Crypto Wealth Manager for everyone. Wallets, exchange, Crypto Robo-advisor, DeFi Earn to lend stablecoins in DeFi, and Crypto Strategies: it is all you need in a Crypto Asset Manager. And it is accessible from 30€.

Our computers do the heavy lifting for you with a long-term perspective so you don't have to. From crypto on-and-off ramps to passive income and diversified portfolios, OSOM has you covered.

If you are wondering how the Autopilot Works, read this. The live performance is here If you want to know why you might want to use DeFi Earn, read this.

The guide to getting started is here.

History of Quantitative Methodology for Portfolio Construction

As the financial world became more complex and diversified, a demand for quantifying market patterns emerged. One of the first economists to supply this demand was the Nobel Prize-winning Harry Markowitz. With his book, "Portfolio Selection," first published in the Journal of Finance in March 1952, Markowitz created the concept of portfolio diversification as we know it.

Under the framework of Modern Portfolio Theory (MPT), investors acquired tools for their investment portfolio management and diversification. With MPT, portfolio construction is based on:

Minimizing risk based on the return ratio or the level of expected risk

How investments affect the entire portfolio instead of viewing it as a collection of individual investments

Among other measures, MPT relies on the statistical tools of correlation and variance. They are employed to calculate the expected return of the portfolio by calculating the weighted sum of each individual asset. MPT became increasingly useful with the rise of ETFs (Exchange Traded Funds).

As indices of individual assets, MPT gives ETF investors the tools to minimize the risk for a given return. Therefore, the variance of the portfolio would also be reduced.

Robert C. Merton

Building upon Markowitz's MPT, the son of the famous sociologist, Robert K. Morton, is the key contributor to quantitative trading strategies. Robert C. Merton won the Nobel Memorial Prize in Economic Sciences for figuring out how to assess the value of derivatives. Together with two other economists - Fischer Black and Myron Scholes - they developed the Black--Scholes--Merton model.

Also commonly called just the Black--Scholes model, it uses differential equations to create a mathematical model of financial markets holding derivatives as investment mechanisms. The model allows for risk minimization by hedging options. If an underlying asset is traded accordingly, it nearly eliminates the risk.

Such hedging has been dubbed as "continuously revised delta hedging," becoming hugely popular with both banks and hedge funds to this day. Of course, nowadays, there are many variations of the model by tweaking its underlying assumptions.

Who or What Are "Quants"?

Altogether, the application of calculus to quantitative finance made it possible to create a quantitative investment strategy that generates excess returns or alpha values. Although the term "quant" was initially reserved for developers of these models, who are usually programmers, mathematicians, and statisticians, it became interchangeable with their models themselves.

This means there are as many quantitative strategies as there are developers who build them. Following the dot-com bubble in the late 1990s, quantitative trading strategies were fully embraced by institutional investors. However, as quants failed to predict the 2008 financial crisis, by not accounting for the effect of mortgage-backed securities, quant limitations became more visible.

Nonetheless, quantitative strategies for portfolio construction have proven their merit over the decades. The most time-tested and popular quants were created by James O'Shaughnessy:

The Trending Value - returned 21.2% annually over a period of 45 years.

Quality-Adjusted Value Microcap - returned 20.3% annually over a period of 34 years.

More modern quants have proven even more profitable. The Qi Value quant has yielded a 710.7% annual return over 16 years. In the same range of returns is the Free Cash Flow Yield and Price Index 12 Months Momentum quant.

Example of Quant-Based Portfolio Management

As you can see, there are dozens of investment strategies to choose from. Each one is based on an angle. For instance, let's say you want to pursue a quant based on its trading volume patterns. Specifically, a quant that establishes a high positive correlation between the asset's price and its trading volume.

Therefore, if an asset's trading volume increases, followed by its price hitting $80 or drops its trading volume when it hits $100, the quant would automatically set a buy at $80.50 and a sell at $100.50. In a similar vein, one can trade with quants based on earnings reports, and any other market dynamics that can be used for algorithmic portfolio construction.

The Rise of Robo-Advisors

Having mathematical models of the market to gain an advantage is one thing, but having them mass-deployed to individual retail traders is another matter entirely. As mentioned previously, before computers became commonplace, quantitative investment strategies were reserved for large financial institutions. After all, it would take teams of analysts to deploy them.

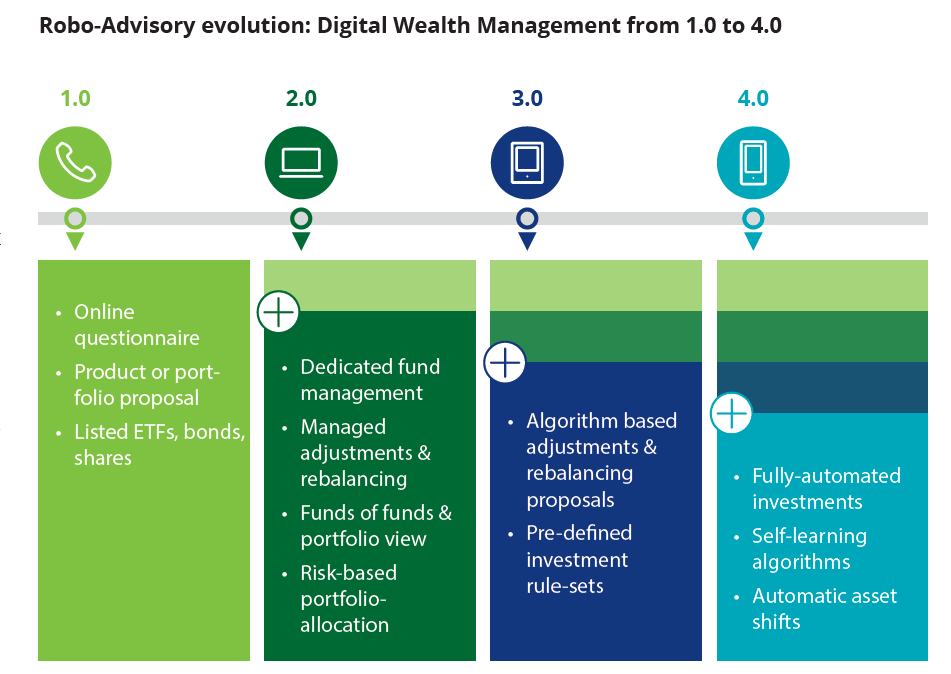

With the dawn of machine learning, it became possible to automate trading strategies and techniques. Hence, the rise of robo-advisors - computer programs that fulfill the role of human financial advisors, including quants. They represent a major shift in how people view finance and how to execute portfolio management.

By replacing humans, robo-advisors drastically reduce the cost of investments - up to 66% in fee reductions alone. From their humble beginnings as online questionnaires to self-learning algorithms, they have evolved significantly within the last two decades.

*Deloitte: *Robo-advisory evolution

Therefore, with the latest generation, robo-advisors have democratized the entire financial industry. Not only do they reduce the cost of high fees, but they make the financial world more accessible to those who don't have time to spend hundreds of hours learning the ins and outs of markets, risk management, and trading strategies.

Interaction with a robo-advisor is a simple process, as the artificial intelligence creates an investor's profile based on answers to some of these questions:

What is your preference on how much money should be earned on the initial investment?

For how long are you willing to wait for the returns on the investment?

Would you like to engage in low, moderate, or high risk trading?

Of course, the foundation to these and other Q&A building blocks for your portfolio management lies on the MPT. Robo-advisors then automate the quant for your portfolio with the least risky one, yielding the lowest annualized compound returns.

Needless to say, modern robo-advisors represent portfolio managers, which are a superior alternative to managing manually, and they come without a need for a costly expert financial advisor. Not only are they built on tried-and-tested economic modeling, but they dynamically adapt to how markets move. According to S&P Global Market Intelligence, robo-advisors currently manage about $1 trillion worth of assets, projected to increase their footprint further.

World Bank, Robo-Advisors: Investing through Machines

In essence, robo-advisors are much like dating apps. Based on your input, they create a profile of your current finances, your needs, wants, and acceptable risks and then find out the best, most profitable strategies to make you money through algorithmic trading. This way, AI-enhanced robo-advisors leave investors with plenty of time to pursue other ventures while they take care of your investment strategies.

As for the cost of running robo-advisors, companies like Vanguard, Schwab, Betterment, and Wealthfront typically charge between 0.15% to 0.5% management fee. With more packed competitive space for robo-advisors, the costs tend to decrease over time. Lastly, they have become very popular for tax harvesting - automated selling of assets, even at a loss, in order to offset capital gains or taxable income.

Advantages of Quant Strategies

Anyone familiar with DeFi, Bitcoin, Ethereum, or other cryptocurrencies is deeply familiar with dozens of chart types and technical indicators. Each one gives an insight into the optimal time to enter and exit the market. And within that space between entering and exiting lie trading profits.

However, even with the most thorough technical analysis, trades can take a nosedive. Such an experience inevitably leaves an emotional imprint, leaving one to guess what went wrong. In turn, this second-guessing creates its own kind of volatility - an emotional one.

Quantitative investment strategies used for portfolio management kill two proverbial birds with one stone. By automating this time-consuming and emotionally draining process, quants leave the foible of emotions outside the trading equation. Likewise, risk-adjusted returns via so-called risk-parity portfolios compensate for the volatility of markets.

More importantly, due to inherent diversification, quants can allow for combining long/short trading strategies. After all, their starting point is a benchmark for a particular market, incorporating industry weighting to construct the mathematical model.

Disadvantages of Quant Strategies

The key disadvantage for quant strategies manifests in the difference between qualitative and quantitative analysis. Unlike the mathematically-based quantatitive approach, qualitative relies on human judgment of the company, its operations, product viability, personnel, and leadership change. When the human mind absorbs all of these factors, it forms intuition.

With that said, it bears keeping in mind that intuition can only exert its value when it is a part of a larger investment plan or trading strategy. Furthermore, when you consider that all the charts and technical indicators in the world are merely approximations of reality, intuition becomes a tool whether one consciously chooses to use it or not.

The 2008 financial crisis clearly demonstrated that one cannot see the whole story with a focus on mathematical modeling alone. This also entails that quant strategies have difficulty tracking markets that have significantly changed from the conditions they were designed for.

Lastly, the more a certain quant is in use to exploit patterns, the more will that pattern be less useful and effective as everyone employs it.

Robos in Crypto

Due to small market caps compared to blue-chip stocks and indices, cryptocurrencies tend to have inherent volatility. The large price movement of various cryptos is difficult to track without staying glued to the screen 24/7. Moreover, the sheer quantity of altcoins (10000+) is a daunting prospect for newcomers who flee near-zero or negative interest rates in the banking sector.

For them, robo-advisors could breach that psychological barrier, just as Canadian Bitcoin ETFs saw an increase in investments by 31% from 2019 to 2020. Likewise, upcoming American crypto ETFs should soon increase crypto exposure to millions of customers, expanding market caps and reducing volatility.

As for how diversified one's crypto portfolio construction should be, Betterment advises not to exceed 10% of the total value of portfolio assets. Further, they suggest diversification across multiple assets and asset classes to make up that percentage.

Where Should You Start Your Portfolio Management?

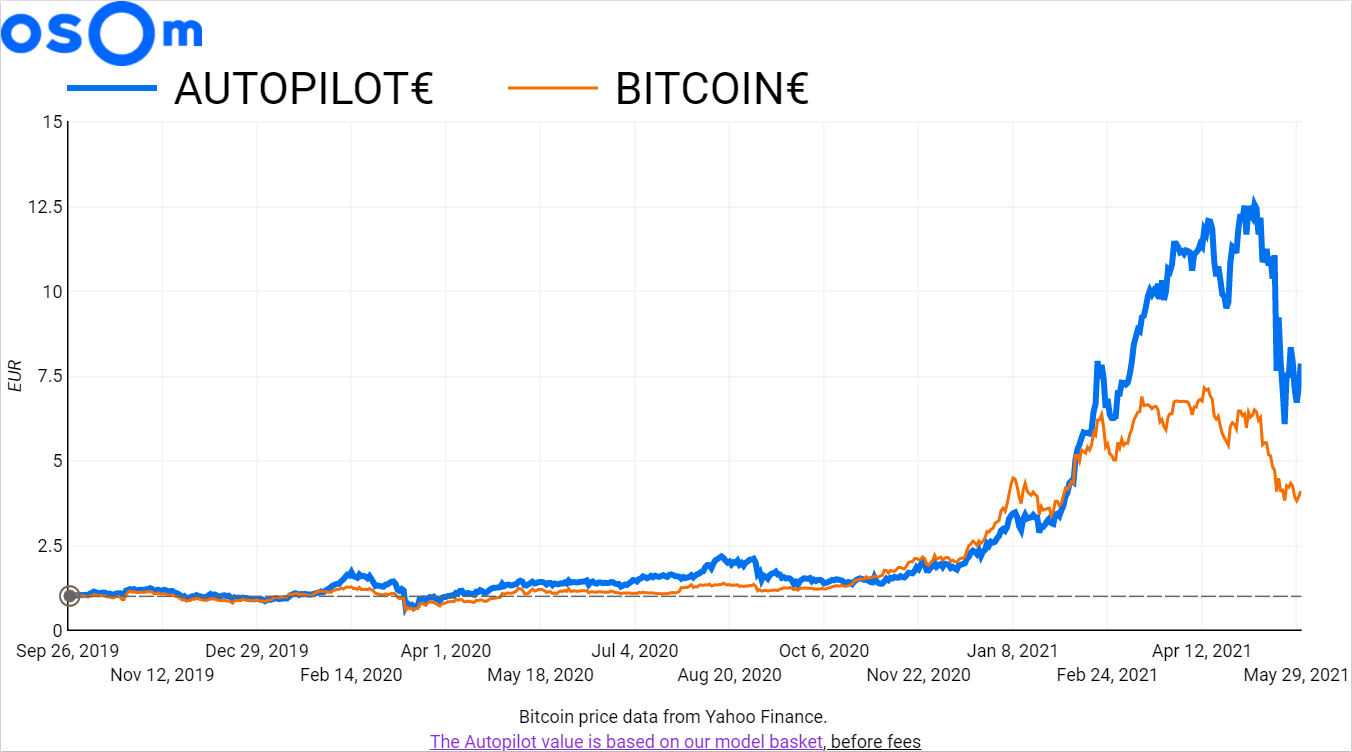

There are few platforms that have even announced they will launch crypto robo-advisors in the near future. Osom fills that gap now for automated crypto management and diversification. Its app-based Crypto Autopilot uses quant strategies to cover a basket of cryptos, all of which are denominated in deflationary Bitcoin (BTC).

Comparable to high-yield stock quant strategies, Osom's pioneering robo achieved 91.56% BTC performance since September 2019. Tapping into historical data of price fluctuations, Crypto Autopilot's algorithm compares it in real-time with the current crypto price.

Furthermore, the crypto basket is void of dud coins - meme coins, low market cap coins, forked coins, and stablecoins. Only those with high liquidity and high market cap can ensure devaluation resilience.

Mathieu Hardy

Would you like to be notified about new posts?

Related articles

Crypto trading bots execute the best possible trades automatically, removing the need for any human intervention.